You can draw at risk by writing a, using a new mastercard, or even in different ways

The period after the fee deadline where this new debtor can pay without having to be hit to possess later charge. Sophistication periods incorporate only to mortgage loans on what interest percentage is calculated monthly. Easy attention mortgage loans do not have an elegance period while the attract accrues every single day.

Home financing on what the percentage goes up by the a constant percent getting a specified number of periods, and after that accounts off to the remainder title and you may amortizes fully. Such as, the fee you are going to improve by the 7.5% all the one year to own 60 days, and after that try constant towards left title from the a good totally amortizing level.

A proposition by HUD for the 2002 to let lenders while some provide packages out of money and you can settlement qualities within one price.

The house Cost Refinance System (HARP) is actually come of the Federal national mortgage association and Freddie Mac this present year so you’re able to provide refinancing to help you consumers with mortgage-to-worth percentages too much to be entitled to the practical apps.

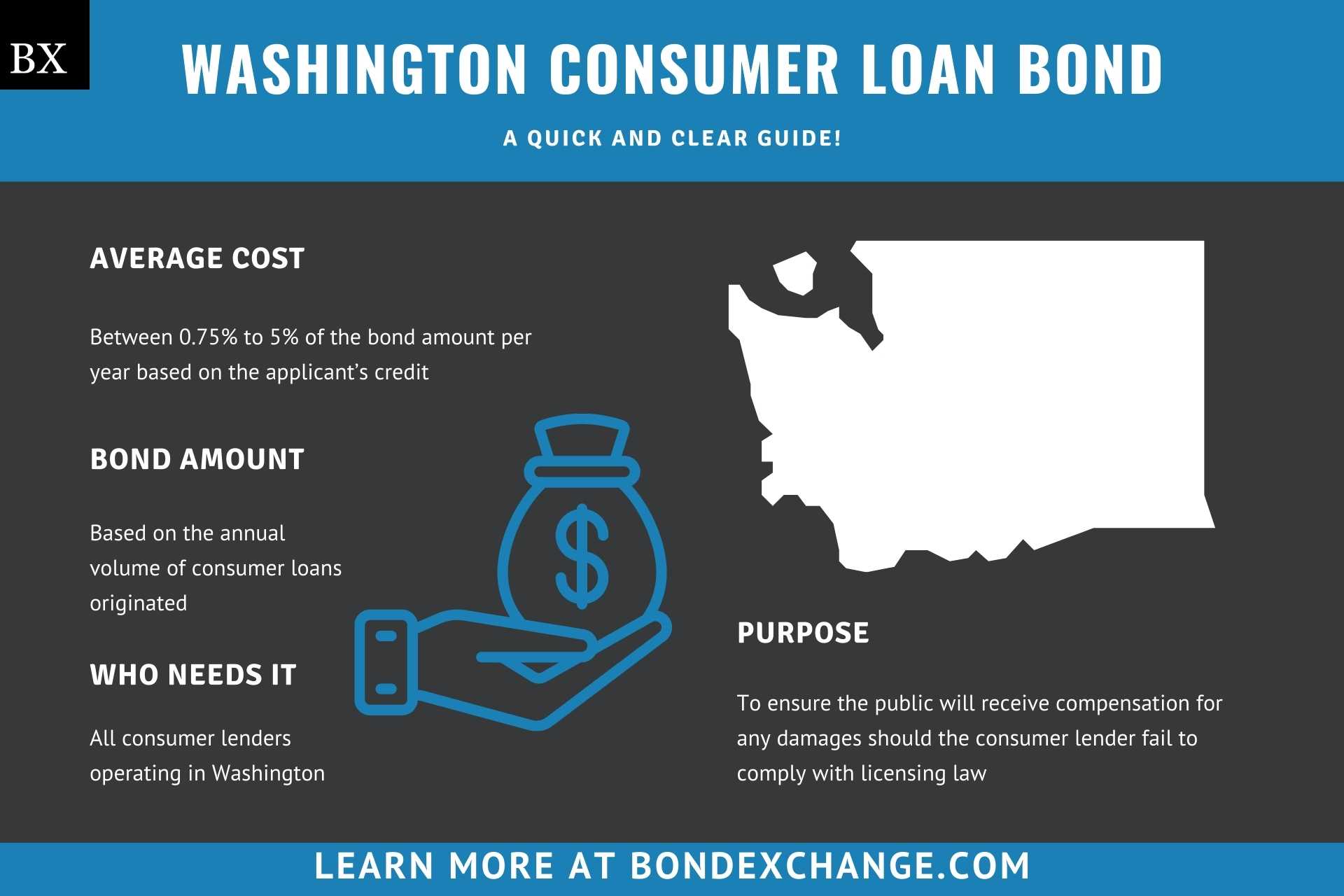

Using a HELOC rather, you obtain this new lender’s pledge to progress you around $150,000, in an amount and also at a time of the opting for

Insurance rates purchased because of the borrower, and you may required by the lender, to safeguard the property facing losings off fire or any other potential risks. Also known as homeowner insurance coverage, this is the second I inside PITI.

Is short for Household Security Transformation Financial, a contrary mortgage program subscribed of the Congress in 1988. To your a good HECM, FHA insures the lending company up against reduction in the big event the mortgage balance within cancellation is higher than the value of the property, and assures brand new debtor you to one costs owed on the lender is made, even when the financial goes wrong.

The belief your list really worth that the speed on the a supply is tied up employs a similar trend such as specific early in the day historic months. Inside fulfilling its revelation debt concerning the Arms, some loan providers show the way the homeloan payment would have changed towards a home loan started a while in the past. That is not very beneficial. Indicating just how a home loan got its start now perform change if for example the directory used a historical pattern could well be helpful, however, no one does it.

The proper execution a borrower get at the closing you to definitely information all of the repayments and invoices one of many parties during the a bona-fide estate transaction, plus borrower, financial online personal loans Colorado, family vendor, mortgage broker as well as other providers

Insurance purchased by borrower, and you will necessary for the lending company, to safeguard the home facing losses out-of flames or other problems. It’s the 2nd I inside the PITI.

A home loan developed since the a personal line of credit up against hence a borrower can be draft so you’re able to a max amount, in lieu of that loan for a predetermined money amount. Such as for instance, using a simple financial you could borrow $150,000, which could be paid in its entirety from the closing.

A guideline approved by Federal national mortgage association and Freddie Mac computer, energetic , the agencies thenceforth do simply purchase mortgage loans that were supported by a keen independent assessment. The rule got particular terrible regardless of if unintended ill-effects.

A federal government-owned or associated property bank. Which have minor exceptions, bodies in the us has never loaned directly to consumers, however, housing banking companies is prevalent in a lot of developing countries.

The sum of homeloan payment, threat insurance policies, possessions taxes, and you may resident relationship fees. Identical to PITI and you will monthly houses bills.

The fresh ratio out of homes bills in order to borrower money, which is used (and the total costs proportion or other factors) into the qualifying individuals.

An arm on what the original rates keeps for some months, where it is fixed-rate, after which will get variable price. Basically, the phrase was applied to Palms having 1st price periods out-of 3 years otherwise prolonged.