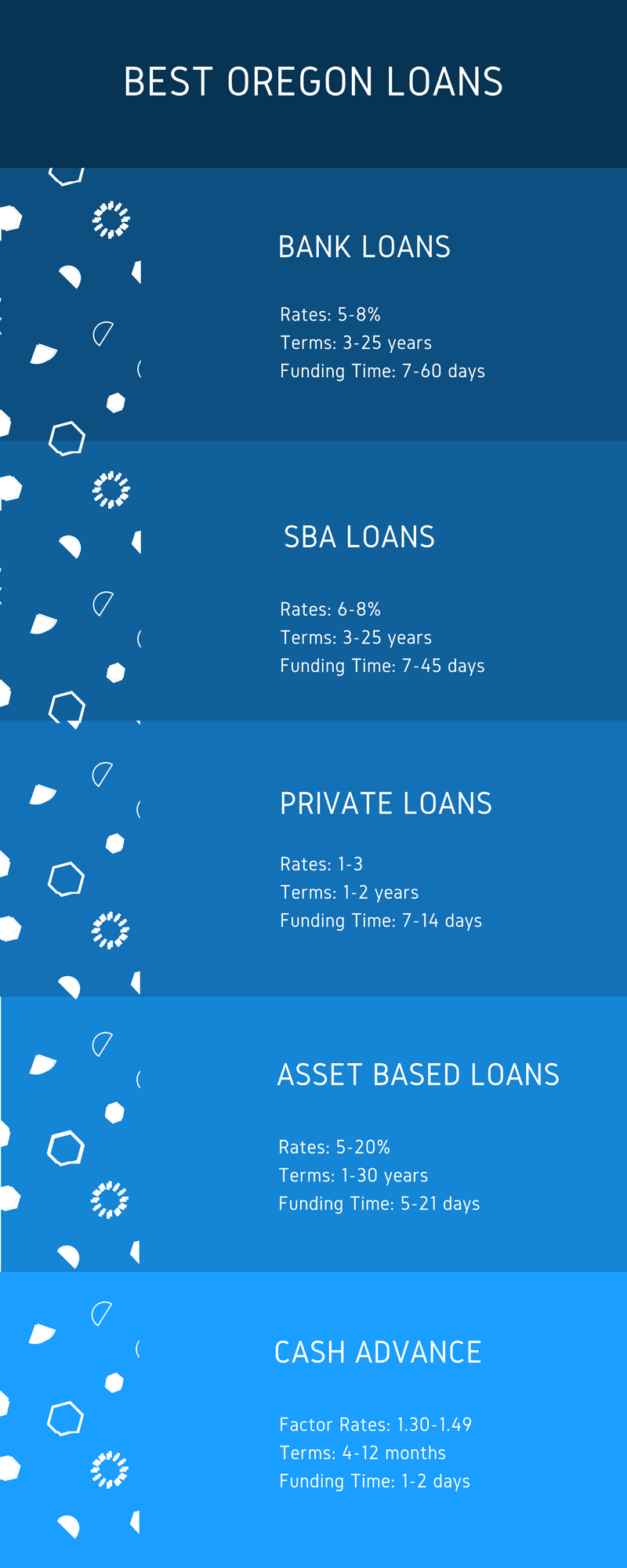

While the a military retiree and a monetary coordinator, I’ve seen first hand how book demands faced by armed forces society enhance changes in the fresh discount and you will U.S. authorities rules.

Into Sept. 18, this new Federal Reserve then followed more substantial-than-requested, 50-basis-area (0.5%) rate of interest slashed, and while of a lot can get regard this owing to an over-all economic contact, I would like to take a moment to adopt how which influences military family, specifically.

From deployments to help you OH personal loans constant actions and you can everything in between, the latest military experience doesn’t usually individually fulfill the civil feel. Here’s how a choice including the Fed’s normally ripple by way of the personal money of your own army society, affecting from coupons account to help you financial prices.

Lower Borrowing from the bank Costs

Among the first things that pops into their heads having a beneficial Given price cut is where it may reduce steadily the cost of borrowing. Of many military family members believe in fund for vehicles, home as well as to pay for unforeseen expenses throughout the a permanent change-of-route (PCS) flow otherwise deployment. That it speed slash you are going to provide particular welcome recovery, nevertheless might not be brief otherwise because impactful as the economic headlines possess you might think. Think about, this new feds cannot lay (otherwise cut) the attention rates both you and I shell out in person: It cut means a rate cut-in terms of what financial institutions shell out so you can borrow funds off their financial institutions, therefore affects whatever you shell out available on the market.

- Mortgages: Many army household, plus exploit, have tried Virtual assistant finance when purchasing a property. These loans offer extreme masters, like no down payment, no personal mortgage insurance coverage and you can competitive interest rates. That have interest levels trending lower, this new month-to-month mortgage payments on the latest fund could be more attractive. Considering my conversations with many individuals, it could be a bit early — the current finance bring a considerably all the way down rate of interest — to generally share refinancing, but if you already have a home loan, refinancing could promote a little action area on the budget. For those looking to purchase, it’s the opportunity to lock in all the way down prices while making homeownership more affordable or perhaps to rating a little more bang for the money.

- Auto loans: I think I will properly point out that Americans such as for instance our very own vehicle, and also the armed forces area may even just take “like” and you can intensify you to to “like.” In any case, all the way down costs indicate minimal automobile financing, which could make a big difference if you are looking to buy a new automobile. This is exactly perhaps the right time to mention the potential economic benefits associated with riding your car or truck a lot of time not in the period of their mortgage.

- Playing cards: If you’re holding credit-cards financial obligation, a speeds reduce could help convenience this new financial burden a while. Many armed forces families trust credit to cover unanticipated expenses, should it be during time-to-date life, a deployment or transitioning from the services. All the way down prices towards playing cards indicate faster attract turning up and an increased portion of their “more-than-the-lowest fee” going towards the the principal harmony.

Down Output on Deals and you will Expenditures

Whenever you are less borrowing from the bank is superb, the fresh drawback is that a speed clipped can also indicate down productivity towards the deals and conventional investments. Due to the fact an economic coordinator, I’ve constantly prioritized strengthening a stronger emergency fund and planning for tomorrow. Regrettably, all the way down rates renders you to definitely a little while much harder and less satisfying.

- Offers profile: We all understand how important its getting a beneficial well-stored emergency fund, particularly considering the uncertainty regarding military existence. But with lower pricing, the money sitting in savings levels produces notably less attention. This might allow a tad difficult to grow one to fund towards the “address peak.” Don’t get too trapped in this thought. The main element is that you feel the crisis discounts available when it’s needed. The Fed reduce can make it all the greater crucial that you buy an informed available rates on your own savings.

- Senior years membership: Of these invested in the newest Thrift Discounts Plan (TSP) and other senior years or financing account, the newest Fed’s speed cut will not really apply to inventory fund abilities, it is determine market conclusion. All the way down prices tend to force the stock market upwards, that is great for these having highest-risk opportunities. not, if you are alot more conventional and you can worried about income expenditures, like many retired people are, straight down pricing is a blended wallet, driving bond pricing large, but focus money and you may income streams straight down.

Housing marketplace

Army group circulate more frequently than civilians, possibly most of the few years, based commands from Uncle sam. You to fact possess usually made me cautious with regards to military group and you may owning a home. Straight down rates of interest make a difference to both investing regarding housing industry, such whenever:

- To purchase a property: When you’re in the industry to invest in, all the way down financial costs is a huge work with. They suggest smaller loans and lower monthly payments. If the greatest line goods inside our spending plan shrinks, that’s a positive. Down rates makes this new imagine homeownership more available, particularly for young families.

- Selling a property: On the flip side, if you wish to promote a house, you could potentially face improved battle while the anybody else attempt to employ out-of lower cost, also. So much more consult could automate this new selling techniques, that is a lovely procedure if you find yourself race resistant to the clock so you can go on to an alternative duty channel and steer clear of the possibility of having one or two home costs. Timing was everything you having army family, and you can decreasing interest levels may help beat stress during a currently chaotic Personal computers.

Inflationary Pressures

One to concern I’ve which have people rate reduce is the possible for this to reignite inflation. If the rising cost of living picks up, it does erode the to acquire energy of your army paycheck. It generally does not seem long because the i fled (otherwise have i?) the problems about this side.

Conclusions

The brand new Fed’s recent fifty-basis-area speed cut gifts each other options and demands. Straight down borrowing from the bank costs brings save, particularly having mortgage loans and you will fund, but diminished productivity into savings and possibility inflation mean we need to sit aware as we screen our monetary package. Military family are durable and you will ingenious, but getting informed and you will adapting so you can change like these try imperative to keeping financial balance.