FICO (originally Fair, Isaac and Team) keeps a credit scoring rates out-of 300 so you’re able to 850

Possibly you are in a discussed life style condition (that is, coping with a grown-up who isn’t your romantic companion) on account of an economic crisis, otherwise you’re an occupant under reduced-than-better situations pining being a citizen.

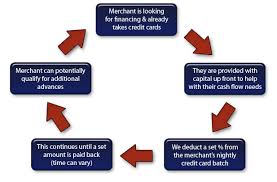

There are other selection on the table compared to those listed above, and additionally what is known as a non-accredited mortgage or non QM mortgage.

Such mortgage is actually for anyone who doesn’t have the desired documents to show he or she is able to make financial payments (and people who have almost every other book items); Another option was a profile loan, which the financial continues a unique balance sheet in place of offering they towards the second home loan field.

Likewise, there are certain county and you can neighborhood programs around readily available for and you can specifically open to basic-day people. These are generally knowledge classes, software to possess factual statements about deposit guidelines programs, and you will courses to help people arrange for home-control even if they’re not able quickly. Gurus say such really should not be thought of as public services but for insights every subtleties out-of financing programs.

In the end, there are groups out there such as NeighborhoodWorks The usa, whoever one purpose would be to create potential for people to live on in the sensible belongings and improve their life.

Their system – composed of more 240 area development groups and you may an existing support build also provides advisors who will be coached and you will certified to provide education so you can potential home buyers. You to education primarily focuses primarily on one’s book monetary products in order to assist them to get to the goal of household-control.

How can Mortgage brokers See Your credit history?

Mortgage lenders play with studies in the about three fundamental credit scoring bureaus: Equifax, Experian, and TransUnion. In relation to obtaining your first domestic client financing might usually glance at the middle credit score of one’s around three. As well as the credit scores, lenders also feedback your credit report, exploring situations like overall financial installment loans for bad credit in Hamilton IN obligation and one factors including non-payments or later payments.

Tips Boost Credit score

Skipped and late costs is reduce your FICO rating. Make certain you build for the-go out money to your all finance and you will credit cards. Setting your account on the autopay is an excellent method to assist using this.

Earliest things very first: not all borrowing from the bank checks damage your credit score. Silky inquiries, such as those used to have criminal background checks, cannot affect your own rating.

Although not, hard inquiries, such as those generated once you apply for another bank card or loan, can be decrease your rating quite. For each and every difficult inquiry can reduce your credit rating of the a few facts. Constantly make certain whether or not the collector perform a challenging or delicate pull-on your credit score.

What is a beneficial Subprime Borrower?

When you have impaired borrowing from the bank and you’re applying for a primary go out home loan, you can even end up being there’s a label connected into application that you can’t reduce – that subprime borrower.

Experian, a major consumer credit revealing business, represent a great subprime borrower since someone whoever credit score perform imply an averagely risky out of inability to repay that loan. Experian lumps those with an effective FICO Rating away from 580 to help you 669 regarding the subprime borrower category, but some other lenders define an equivalent consumers according to their own conditions.

Just what was once the actual situation is that subprime borrowers was basically faster acquainted the loan processes. Subsequently, they certainly were less likely to choose most useful financial cost, and less likely to be offered option subprime financial conditions and applications. Subprime borrowers was basically posts into getting accepted to acquire a house that have poor credit.