Within the 2012, Wells Fargo reached a beneficial $175 billion settlement into the Justice Company to pay Black and you may Latinx borrowers exactly who eligible for funds and was in fact energized high fees otherwise costs or improperly steered toward subprime money. Most other banking institutions together with paid agreements. Nevertheless injury to categories of colour was long-lasting. People not simply missing their houses nevertheless opportunity to recover the capital whenever homes cost plus mounted back-up, adding once again to your racial wide range gap.

During the , the Government Set aside revealed that an average Black and you may Latina otherwise Latino houses earn approximately half as much as the typical White house and you can individual only about 15% in order to 20% as often online wide range.

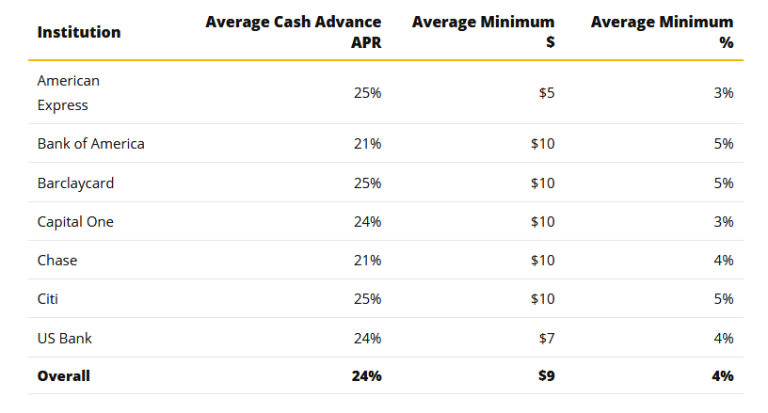

Payday loans

Brand new payday loan business gives vast amounts of dollars annually within the brief-buck, high-rates fund while the a link to another location payday. This type of finance normally is actually for a fortnight, which have annual fee costs (APR) ranging from 390% to help you 780%. Pay check lenders services on the internet and thanks to storefronts largely from inside the economically underserved-and you will disproportionately Black colored and you will Latinx-neighborhoods.

Even though the government Realities when you look at the Credit Work (TILA) needs pay day lenders to reveal its loans fees, most people disregard the will cost you. Extremely funds try to possess 1 month otherwise less which help consumers to generally meet quick-name liabilities. Financing number throughout these financing usually are out-of $100 in order to $step 1,000, which have $500 are popular. The financing usually can be folded more than for additional funds charges, and many consumers-of up to 80% of those-end up as repeat people.

With the fresh charge extra when a quick payday loan is refinanced, the debt can merely spiral unmanageable. An excellent 2019 investigation learned that playing with payday loan doubles the pace away from case of bankruptcy. Many legal cases was basically submitted against pay day loan providers, as financing regulations have been passed because the 2008 economic crisis to produce a more clear and you can reasonable lending market for consumers. However, look shows that new and that it appreciated a boom through the the latest 20202022 COVID-19 pandemic.

If a lender tries to rush you from approval process, does not reply to your concerns, otherwise ways your use more money than simply you really personal bad credit loans Michigan can afford, just be wary.

Auto-Identity Money

Talking about single-percentage finance based on a percentage of car’s worth. They carry high-rates and a necessity at hand across the car’s label and an extra group of keys since guarantee. With the more or less one out of five individuals who possess its vehicles captured as they are incapable of pay the mortgage, it’s not just a financial loss but may and additionally jeopardize supply so you can efforts and you can child care to possess children.

The Different Predatory Credit

The fresh new schemes was appearing regarding therefore-called concert cost savings. By way of example, Uber, the ride-revealing service, accessible to a great $20 billion payment on the Government Trading Commission (FTC) inside the 2017, partly having automobile financing that have dubious borrowing words that the platform extended to its vehicle operators.

Elsewhere, of several fintech enterprises was opening items called “purchase now, shell out later on.” These things are not always clear on the charges and you can interest rates that will bring in consumers to-fall for the a debt spiral they will not be able to escape.

To safeguard people, of many states keeps anti-predatory lending statutes. Some claims have banned pay check credit entirely, although some has actually lay hats on the count lenders can charge.

This new You.S. Company out of Casing and Metropolitan Creativity (HUD) additionally the User Monetary Shelter Agency (CFPB) also have removed steps to combat predatory lending. But not, while the moving on stance of the second department suggests, rules and you may protections try susceptible to alter.

When you look at the , the fresh CFPB issued a last code creating stricter laws on underwriting out of pay check and you may vehicles-label finance. Following, lower than the new frontrunners within the , the brand new CFPB terminated that signal and you will postponed other methods, a lot more weakening government user protections facing these predatory loan providers.